Funnel account: a subtle signal that can reveal an entire trafficking network

A funnel account rarely looks dramatic at first glance. It may begin with scattered deposits,ordinary payment activity, or a customer profile that appears commercially plausible. But when those transactions start converging into the same account - across branches, cities, or countries- the pattern can point to a much larger network. This article explains how the pattern works, why it remains easy to miss, how published guidance has described it over time.

By Rachid CHIHANI Co-founder Thinsaction — March 2026 · 6 min read

Why funnel accounts matter

A funnel account is not defined by a single transaction. It is defined by the shape of the flow. Funds arrive from multiple points and are then concentrated into one account, often with unusual speed.

The account may belong to an individual, a shell company, or an apparently legitimate business. What makes the pattern important is not simply the amount of money involved, but the structure behind it: many actors feeding one node, then one node sending value onward.That is why funnel accounts matter well beyond transaction monitoring.

They can reveal logistics,coordination, and division of labor inside a larger criminal ecosystem. One person collects. Others deposit.Another party moves the funds. In some cases, the account becomes the financial hinge between street-level cash collection and cross-border trade payments.

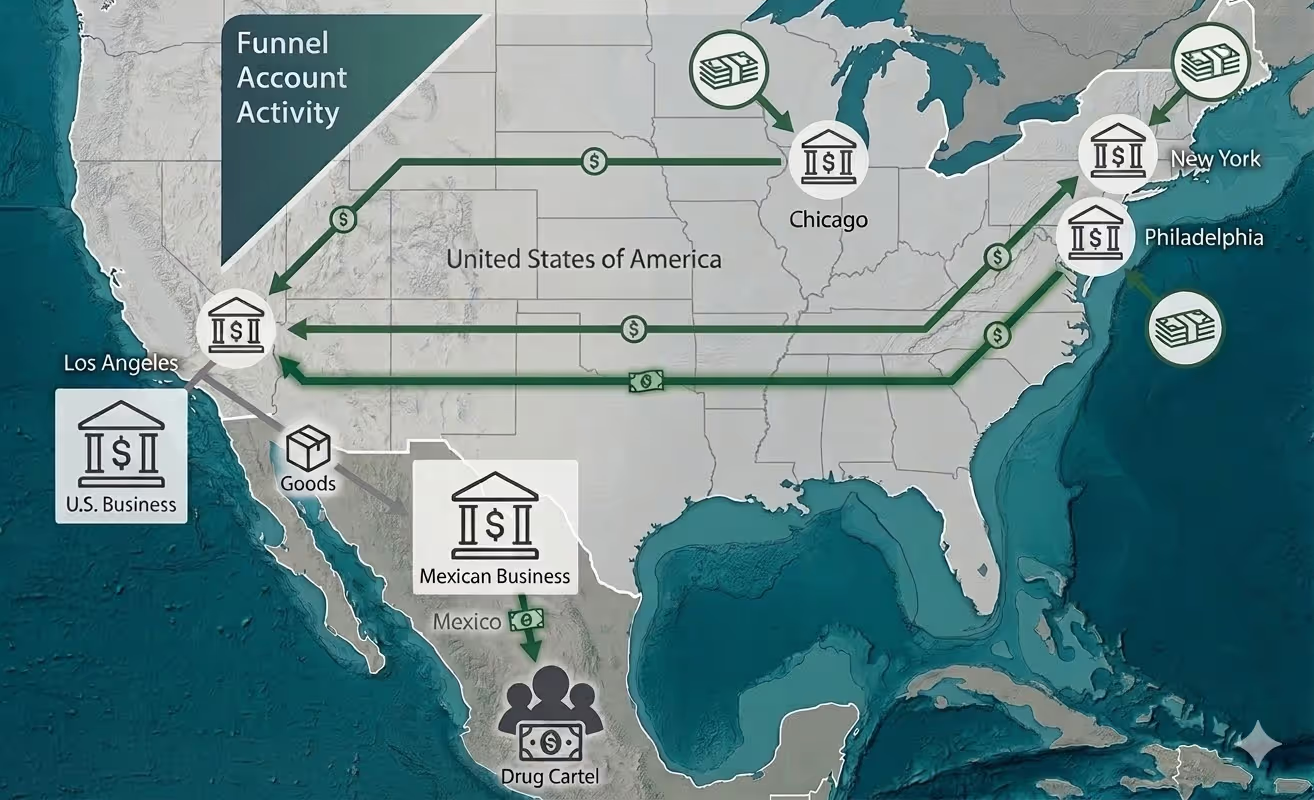

FinCEN's 20141 advisory describes the classic pattern as an account in one geographic area receiving multiple cash deposits - often below reporting thresholds - with the funds then withdraw in another geographic area after little time has passed. The same advisory notes that, in some cases, several funnel accounts feed a single consolidated account. That point is especially important because it shifts the analysis from an isolated suspicious account to a network view.

Figure 1. A classic illustration of funnel account activity converging into a business account and connecting to trade flows1.

How the pattern works in practice

The operational logic is simple. Cash is generated in different places. Instead of moving that cash physically all the way to the final destination, the network deposits it locally into the same account or a small cluster of linked accounts.

From there, the funds can be wired, transferred, converted into checks, or used to pay commercial counterparties. Seen one transaction at a time, the activity may look ordinary. Seen together, it forms a concentration pattern.

Published guidance repeatedly highlights the same practical clues: deposits made far from the customer's footprint; depositors who seem disconnected from the stated business; transaction values that remain just below formal thresholds; and outgoing payments that do not align with the customer profile.

The challenge is that none of these clues is decisive alone. The signal only becomes strong when timing, geography, and counterparty relationships are read together.

This is also why funnel accounts are often described as a low-visibility signal. They do not always announce themselves through one obviously suspicious transfer. They emerge when scattered events are stitched back into a pattern.

What the published guidance keeps pointing to

Several recurring signals can point to funnel account activity2,3. One of the first is deposits outside the customer’s normal footprint. When cash is coming in from places that do not match where the business says it operates, that geographic mismatch deserves attention.

Another common signal is multiple small deposits into one account. On their own, these deposits may look ordinary. But when they accumulate into the same destination account, fragmented activity can become meaningful volume while attracting less attention than a few large transfers.

A third pattern is fast onward movement. In these cases, the account does not behave like a place where funds are held. It behaves more like a transit point, with money arriving and then moving out quickly.It is also important to look at outgoing payments that do not fit the business story. The debit side of the account may connect to sectors, countries, or counterparties that are inconsistent with the customer’s declared activity.

From one account to a wider network

This is the point where a good analyst stops asking only, 'Is this account suspicious?' and starts asking, 'What role does this account play?' A funnel account often sits at the center of a workflow. It receives value from several points, concentrates it, and then redirects it toward another layer of the network. That central position makes it analytically powerful. If you understand the account, you may understand the routing logic of the broader system.

The literature is especially useful here because it shows that funnel accounts are rarely just about cash concentration. They may be linked to trade payments, to the use of intermediaries such as money brokers, or to cross-border settlement mechanisms that give illegal proceeds a more legitimate commercial appearance.

Recent FinCEN material4 shows that funnel accounts still matter in current criminal typologies. They continue to appear in reporting linked to structuring, bulk cash movement, and wider transnational networks. That continuity matters because it confirms that this is not an old pattern that disappeared, it is a durable methodthat adapts.

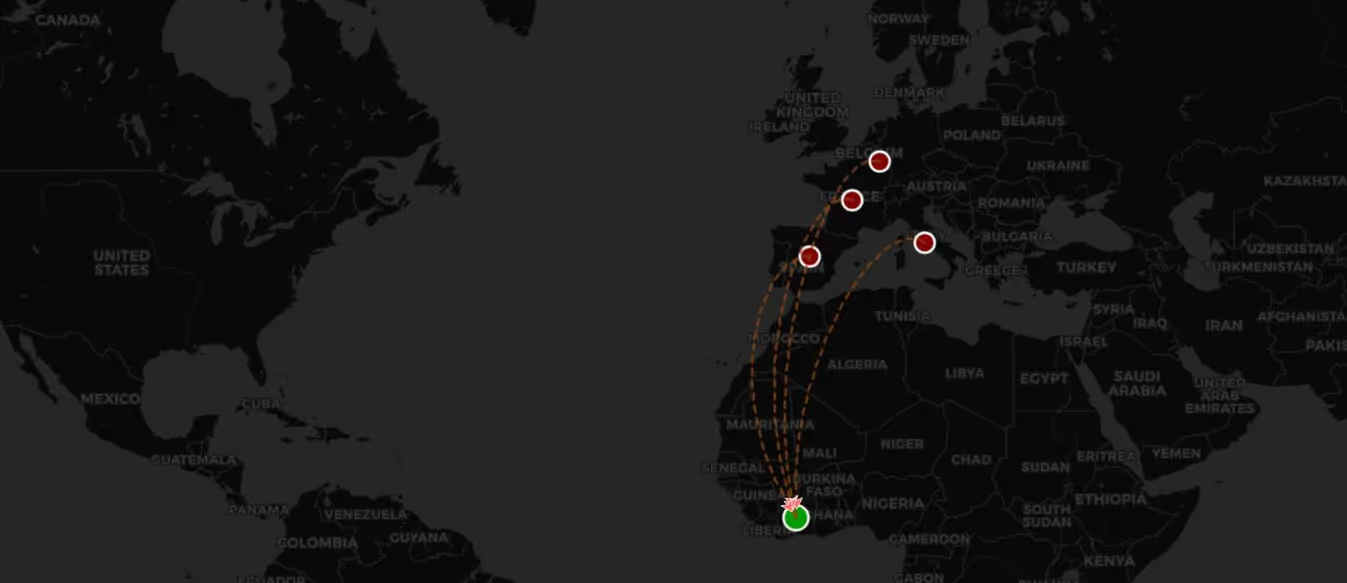

Figure 2. A many-to-one funnel pattern, with several origin points converging into a single account.

The mirror image: inverse funnel accounts

The inverse pattern is just as important. Instead of many points feeding one account, one account distributes funds to many destinations. This can indicate a payout hub, a coordination account, or a redistribution layer used after funds have already been consolidated. If the classic funnel account is about concentration, theinverse funnel account is about dispersion.

In practice, both patterns can exist in the same network. Funds first converge through a funnel account, then fan out through another account to suppliers, intermediaries, local collectors, or destination nodes in several jurisdictions. Looking only for one direction of flow can therefore miss half the story.

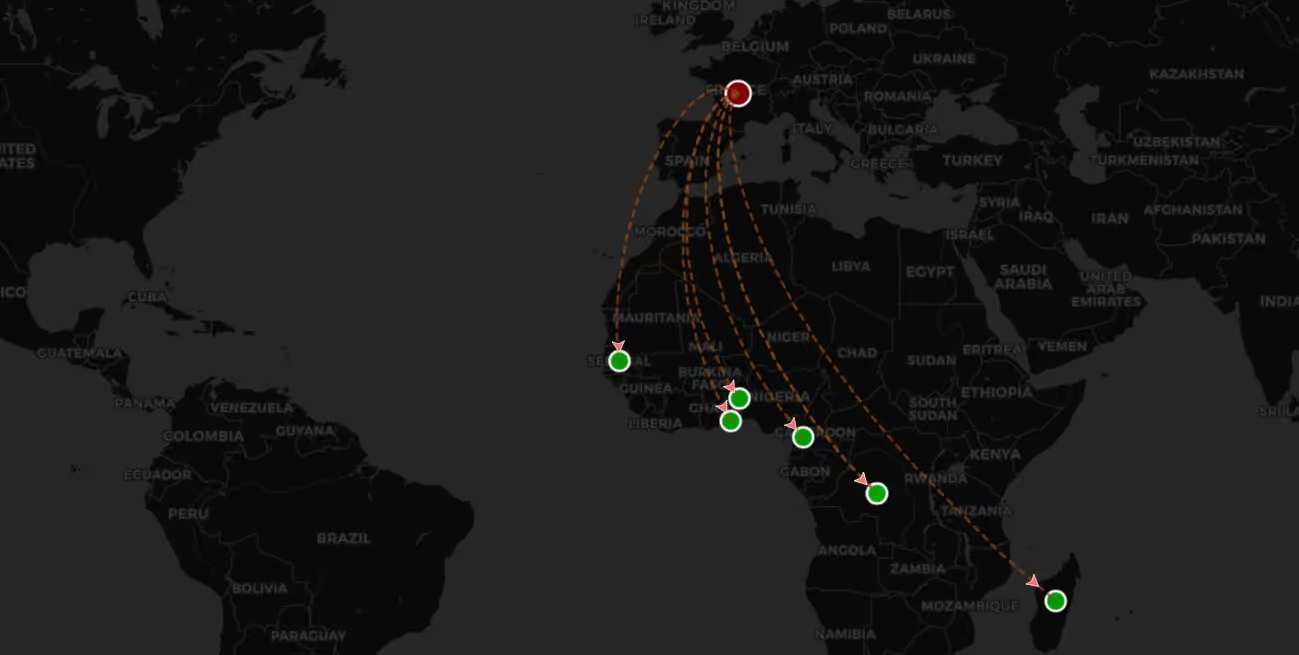

Figure 3. An inverse funnel pattern, where one account distributes funds to multiple destinations.

Turning a weak signal into an investigation lead requires moving from the account to the network. From the single node to the cluster around it. From the transaction list to the structure those transactions form.

That progression — from isolated event to connected evidence — is what separates a compliance alert from an actual investigation lead.

Sources consulted:

[1] FinCEN, Update on U.S. Currency Restrictions in Mexico: Funnel Accounts and TBML (FIN-2014-A005),2014.

[2] FinCEN Advisory FIN-2012-A006 on out-of-state funnel account activity.

[3] FATF, Trade-Based Money Laundering and related guidance on risk indicators and trends.

[4] FinCEN Alert on Bulk Cash Smuggling and Repatriation by Mexico-Based Transnational CriminalOrganizations, 2025.