The $10 Billion Blueprint That Moved to Your Network

How the Mirror Transaction Pattern Migrated from Investment Banks to Peer-to-Peer Transfer Infrastructure

By Achraf EL OUALI — April 2026 · 8 min read

In January 2017, Deutsche Bank paid 631 million in regulatory fines for helping clients move $10 billion out of Russia, undetected, for three and a half years.

The clients were not hiding in some obscure offshore corner. They were Russian nationals facing a specific, concrete problem: their money was trapped.

Russian capital controls restrict the free movement of rubles. Wealth accumulated domestically, through business, through proximity to power, cannot simply be wired abroad. It needs a mechanism. A legal-looking one.

The mirror trade was that mechanism. Buy an asset in rubles inside Russia. Sell the identical asset for dollars outside Russia. Let the asset be the bridge. What enters as trapped local currency exits as freely transferable foreign funds, dressed as the proceeds of a legitimate securities transaction.

No profit on the trade itself. The trade is the cost of extraction.

The fines were paid. The pattern was documented. And then it moved, not to a different bank, but to a different type of network entirely. One with less oversight, lower thresholds, and transaction volumes that make institutional equity desks look slow.

The Deutsche Bank case involved equities, trading desks, and clearing houses. It is tempting to file it under capital markets fraud and consider it irrelevant to money transfer operators, mobile money platforms, and P2P networks.

That would be a mistake.

Strip the pattern to its structural requirements. A mirror transaction needs exactly three things:

No equities required. No trading desk. No clearing house.

Those three conditions exist in every P2P transfer network operating today.

The palindromic structure is identical. What changes is the context.

The same loop running at lower value, higher volume, across mobile money corridors, is structurally indistinguishable from what Deutsche Bank processed for 3.5 years.

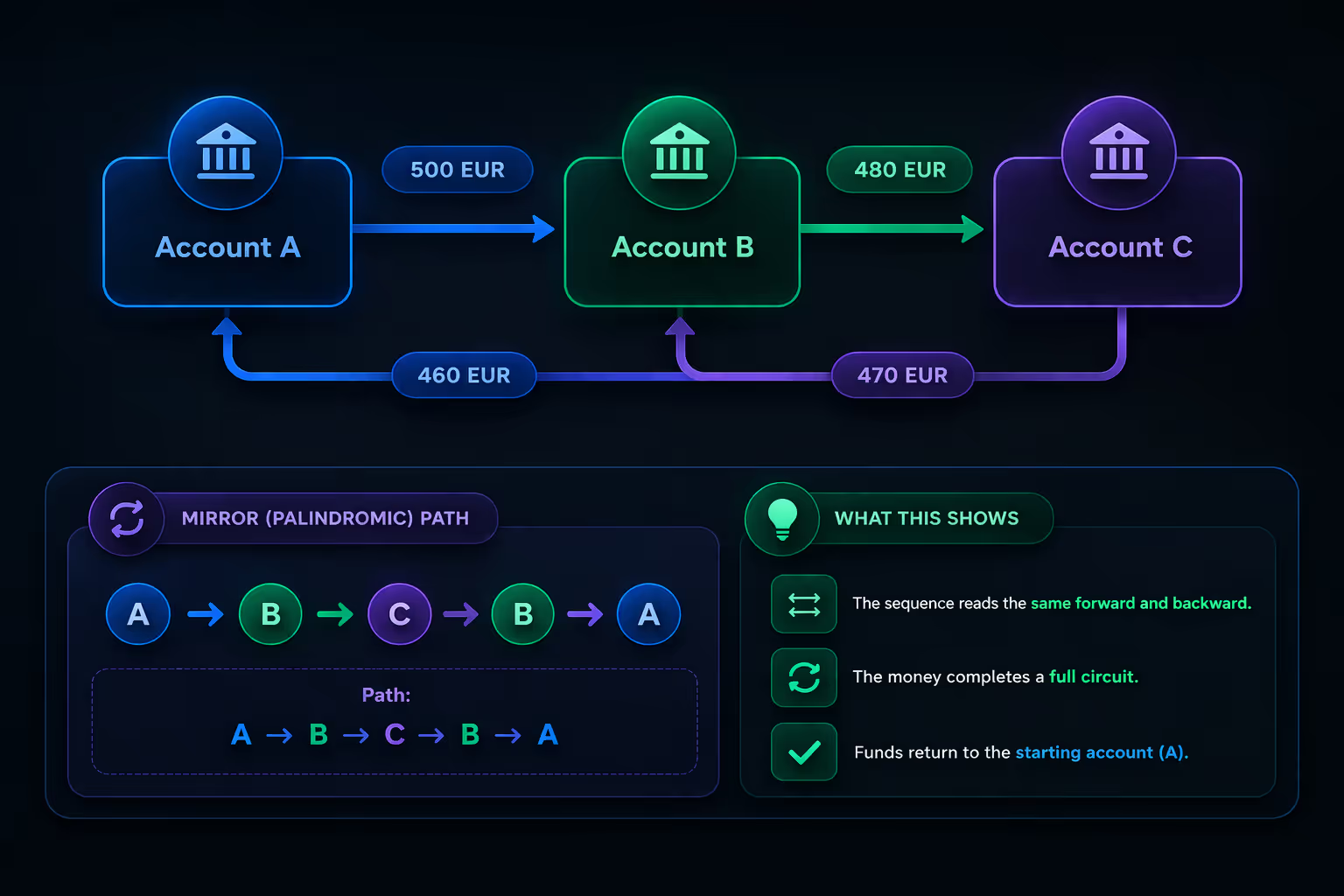

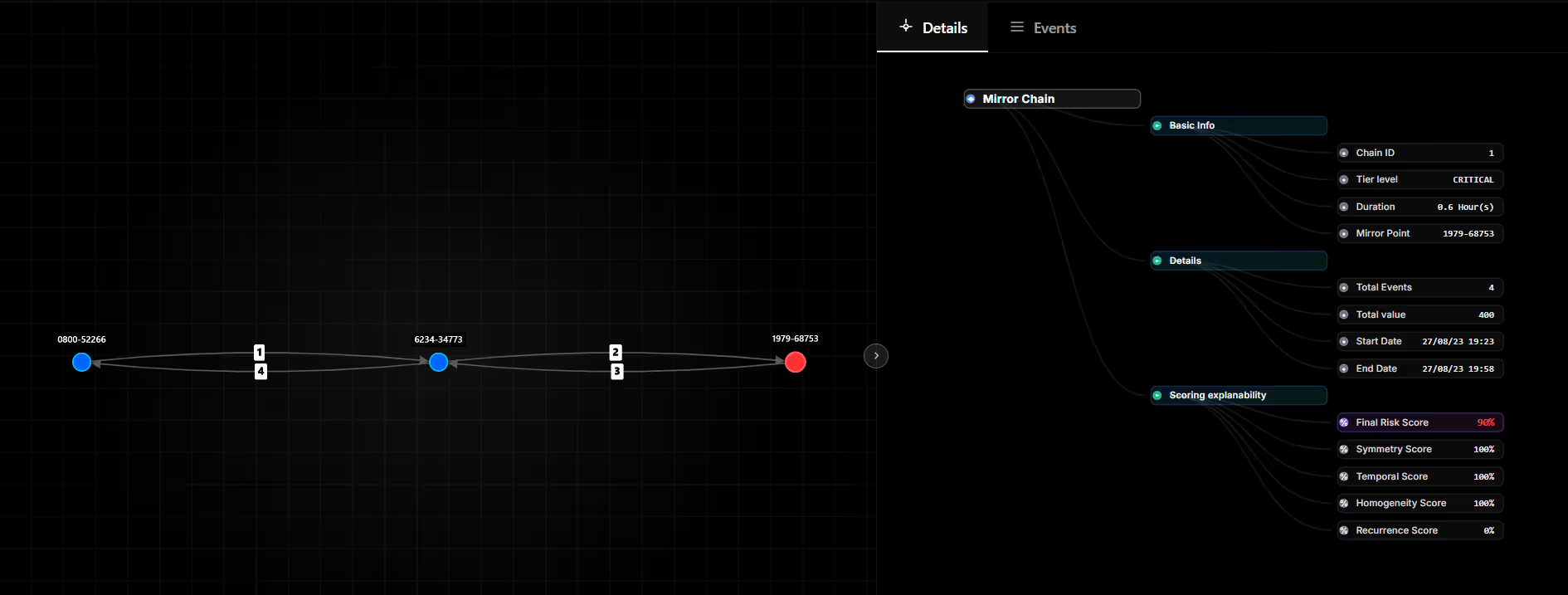

In a transaction log, a mirror chain in a P2P network appears as normal activity.

In tabular form, this is four rows across potentially different time windows. In a graph, it is a single structure with a measurable shape, a palindromic path with a mirror point at C.

Four signals identify this pattern in transfer data:

A single loop is a coincidence. Fifty loops on the same path is an infrastructure.

Deutsche Bank had compliance teams, internal audit, and a legal department. It had 100 internal alerts, and ignored every one of them.

Most money transfer operators have rule-based monitoring systems calibrated to catch individual suspicious transactions. They are not designed to detect relationships between transactions across accounts, directions, and time.

Three gaps make P2P infrastructure more exposed than the institutional environment where this pattern was first documented:

FATF's 2021 guidance on Trade-Based Money Laundering explicitly identifies zero-economic-benefit offsetting transactions as a primary risk indicator, regardless of network type. FinTRAC's 2025 operational guidance extends mirror transaction indicators to money service businesses. AUSTRAC lists bilateral flow symmetry as a documented typology for remittance platform monitoring.

The pattern is named. The obligation to detect it exists.

Deutsche Bank's $631 million fine was a post-mortem. The pattern had already run its course before a single regulator saw the full picture.

In P2P networks, the infrastructure gap is wider. The volumes are higher. The beneficial ownership controls are weaker. And the detection systems were built for a different threat model.

The blueprint was published in 2017. The question is whether it found a new home in your network before you built the capacity to see it.

© Thinsaction 2026 — No part of this article may be reproduced without attribution.